Hafiza Ayesha Waheed

Hafiza Ayesha Waheed

Making Tax Digital has a talent for making otherwise sensible business owners feel as though they have missed an important memo. One letter from HMRC says you need software. Another article says quarterly updates. A software provider says you are already covered. Your accountant says it depends. The result is not clarity. It is low-grade panic.

This guide is for the business owner who wants one straight answer in plain English. It explains what Making Tax Digital actually is, which version applies to you, what the real deadlines are, what software you need, what the penalties look like, and how to get compliant without turning tax admin into a second job.

What Making Tax Digital Actually Is

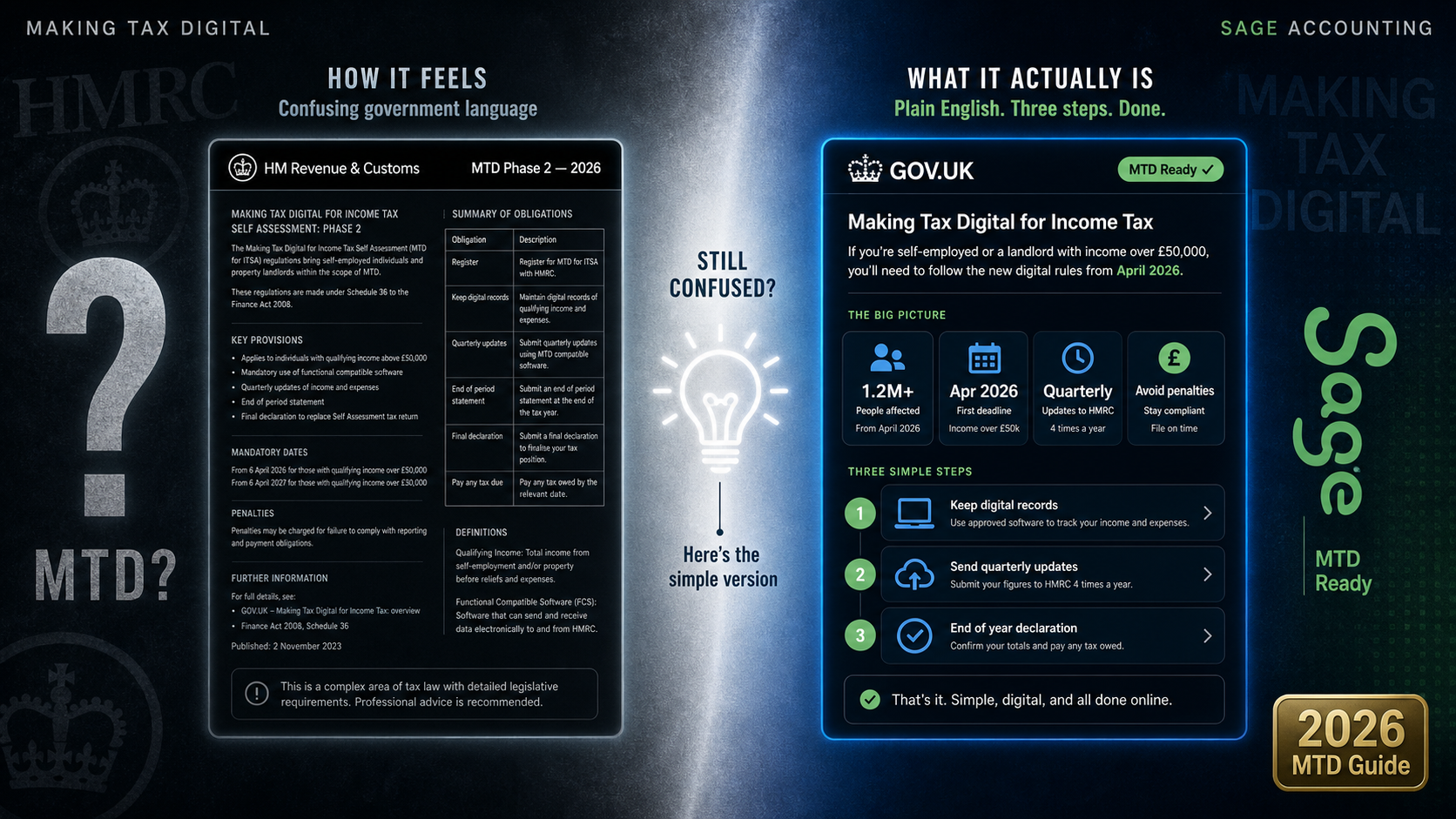

Making Tax Digital, or MTD, is HMRC's long-running programme to move tax reporting away from paper records, year-end scrambling, and manual submissions into digital record-keeping and software-based filing. The principle is simple enough: keep your records digitally as you go, then send updates and returns to HMRC through compatible software rather than keying figures into a government portal.

The trouble is that people talk about MTD as if it were one single rule. It is not. It is a bundle of separate rules introduced in phases. MTD for VAT is already established. MTD for Income Tax is the part now expanding in 2026. MTD for Corporation Tax is not yet mandatory. Most confusion starts when those three get blurred together.

The most useful way to think about MTD is this: it is less a new tax than a new operating system for staying compliant. If your records are tidy, digital, and updated regularly, MTD is manageable. If your system is a bank statement, a folder of receipts, and a burst of activity every January, MTD feels far more threatening than it actually is.

MTD for VAT

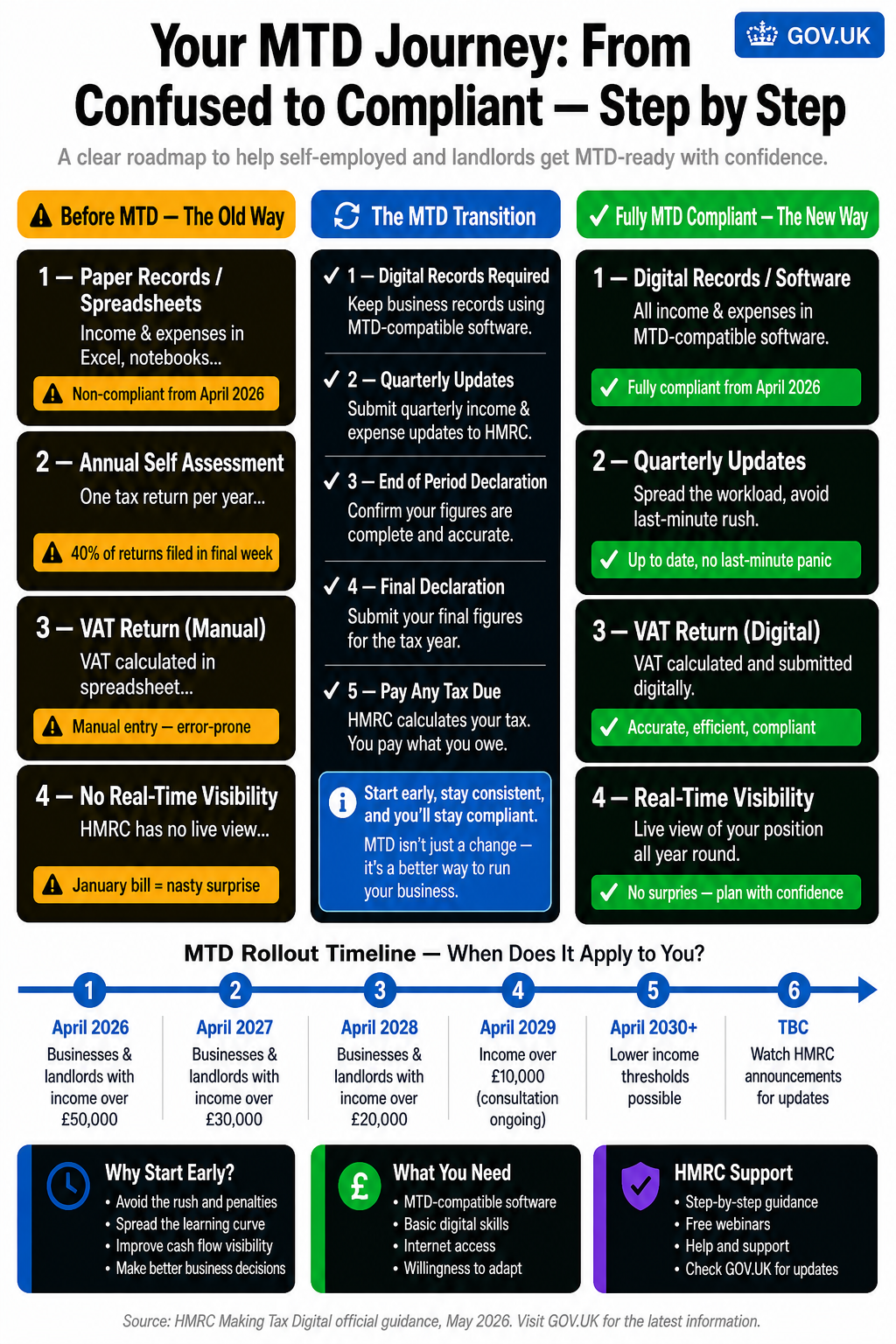

If you are VAT-registered, you are already in the Making Tax Digital world whether you think about it that way or not. Since April 2022, all VAT-registered businesses have needed to keep digital VAT records and submit VAT returns through compatible software rather than the old VAT online service.

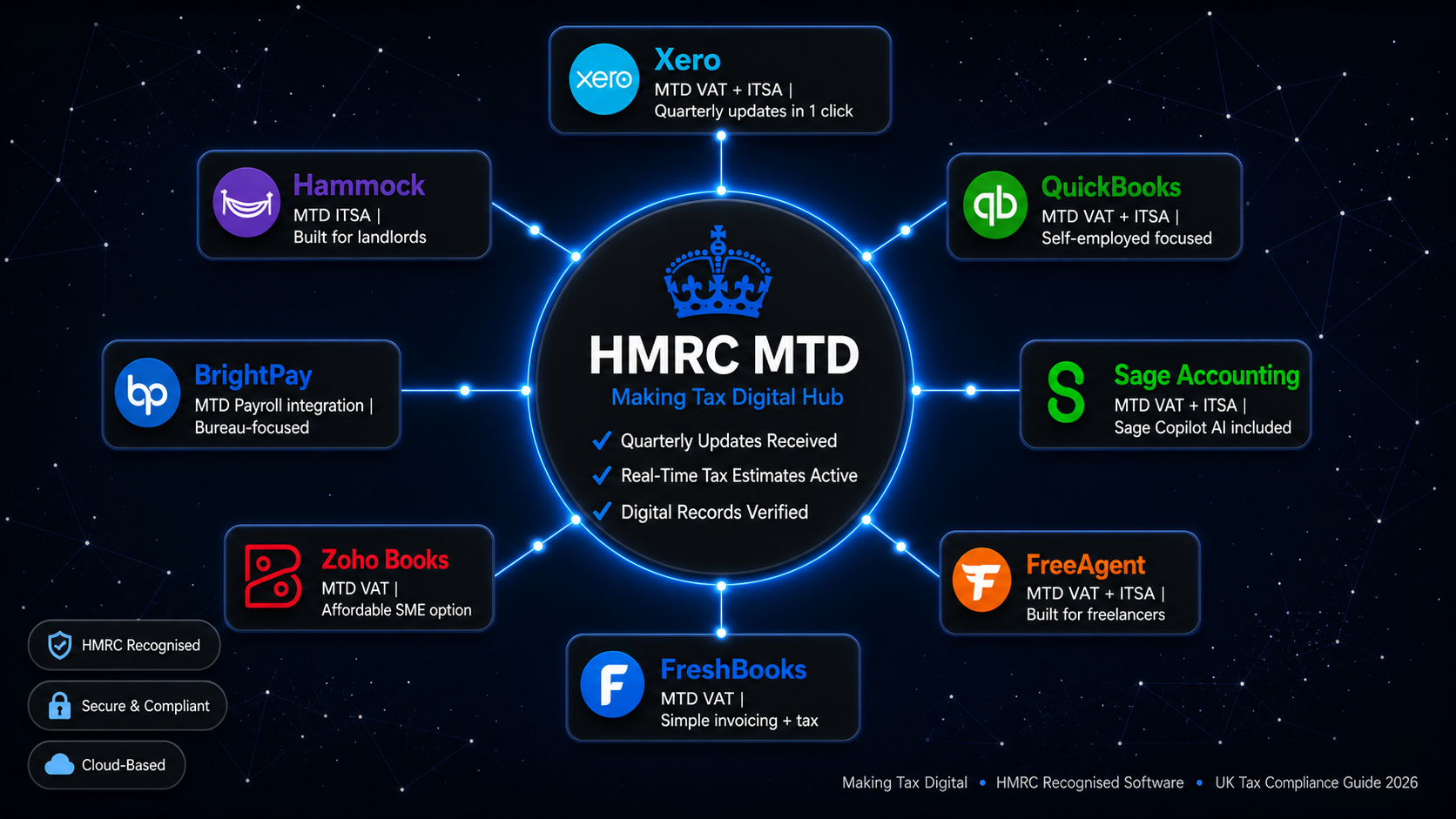

For many businesses, this part is already bedded in. If you file VAT through Sage, Xero, QuickBooks, FreeAgent, or another HMRC-recognised system, you are very likely already compliant. The software pulls the numbers from your records and sends the return to HMRC digitally. That is the workflow HMRC wants.

The catch is the digital link rule. A business that keeps figures in a spreadsheet, manually re-keys totals into another system, and then submits from there may still be breaking the rules. HMRC wants an unbroken digital chain from record to submission. Bridging software can solve that problem, but it is best seen as a workaround rather than a future-proof system.

MTD for Income Tax

This is the part that is making sole traders and landlords nervous, and with good reason: it changes the rhythm of tax compliance. From 6 April 2026, individuals with qualifying income over £50,000 from self-employment, property, or both need to use MTD for Income Tax. That threshold then drops further in later phases.

Who | Qualifying Income | Mandatory From | What Changes |

|---|---|---|---|

Sole traders & landlords | Over £50,000 | 6 April 2026 | Digital records, quarterly updates, end-of-year filing through software |

Sole traders & landlords | Over £30,000 | April 2027 | Same MTD Income Tax process applies |

Sole traders & landlords | Over £20,000 | April 2028 | Same MTD Income Tax process applies |

Limited companies | All levels | Not yet confirmed | MTD for Corporation Tax remains separate and not yet mandatory |

Qualifying income is the part many people misunderstand. It is not your profit after expenses. It is your gross income from self-employment and property combined. So if you bring in £36,000 from freelance work and £18,000 in rental income, your qualifying income is £54,000 and you are in scope from April 2026 even if your actual profit is much lower after costs.

Your salary from employment does not count towards this threshold. Nor does dividend income from a limited company in the same way. HMRC is looking specifically at income from self-employment and property, which is why two people with similar total earnings can have very different MTD obligations.

Quarterly Updates

This is where the phraseology makes the whole thing sound worse than it is. Quarterly updates are not four full tax returns. They are not four tax bills. They are periodic summaries of your income and expenses sent to HMRC through your software so that your records stay current throughout the year.

At the end of the year, you still complete the year-end process through software. That includes finalising the figures and submitting the final declaration by 31 January following the end of the tax year. In other words, MTD spreads the admin out. It does not multiply the tax itself.

The distinction that matters

Quarterly updates are about keeping records current. They are not four extra tax returns and they do not mean four separate tax payments. The year-end deadline for finalising your tax position still matters just as much as it always did.

Quarter | Period Covered | Deadline | What You Send |

|---|---|---|---|

Q1 | 6 April to 5 July 2026 | 7 August 2026 | Summary of income and expenses for the first quarter |

Q2 | 6 July to 5 October 2026 | 7 November 2026 | Second quarterly update |

Q3 | 6 October 2026 to 5 January 2027 | 7 February 2027 | Third quarterly update |

Q4 | 6 January to 5 April 2027 | 7 May 2027 | Fourth quarterly update |

Year-end filing | 2026/27 tax year | 31 January 2028 | Final declaration through MTD-compatible software |

That schedule matters for one practical reason above all others: if you are used to sorting everything once a year, MTD forces a change in habit. Businesses that reconcile monthly or at least quarterly will adapt quickly. Businesses that leave bookkeeping until panic season will feel every deadline as a fresh shock.

What Software You Need

HMRC does not provide the software itself. It provides the rules and the connection points. You need compatible software that can keep digital records, send quarterly updates, and submit your year-end information directly to HMRC. That is non-negotiable once you are in scope.

In practice, that means choosing a platform that is not merely popular, but actually suitable for the kind of business you run. A landlord with a handful of properties has different needs from a sole trader sending dozens of invoices a month. A contractor with CIS complications needs something more robust than a minimalist bookkeeping app. MTD compliance is the starting point, not the full buying decision.

This is where Sage has a particularly strong angle. For sole traders and landlords, Sage offers free MTD-ready options that are clearly positioned around Income Tax compliance rather than treating it as an expensive upgrade. That matters because the emotional resistance to MTD is often not the admin itself. It is the feeling of being pushed into a recurring software bill just to satisfy HMRC. A free entry route changes that conversation completely.

You need software that is HMRC-compatible for the exact tax obligation you are dealing with, not just software that handles bookkeeping in general.

You need digital records kept throughout the year, not a year-end dump of totals.

You still need to sign up through HMRC where required; software alone does not automatically enrol you into every part of MTD.

If you already use Sage for bookkeeping, moving into MTD is usually more a workflow adjustment than a full systems change.

If you are choosing from scratch, simplicity matters more than feature bloat; the best MTD setup is the one you will actually keep up to date.

Penalties

HMRC has moved to a points-based penalty system for late submissions under MTD for Income Tax. Miss a deadline and you receive a point. Reach the threshold for your filing frequency and a financial penalty is triggered. For quarterly obligations, that threshold is four points. Hit it, and the fine is £200. Keep missing deadlines after that, and more £200 penalties can follow.

That sounds severe, but there is a practical nuance: the first year has been designed to help businesses adjust. There is a soft landing on quarterly update penalties in 2026/27, which takes some immediate sting out of the transition. That should not be read as a reason to drift. It should be treated as breathing room to get your systems right while the stakes are temporarily lower.

The bigger risk is not usually one missed quarterly update. It is bad habits hardening into a pattern. Once a business gets behind on record-keeping, every new deadline becomes harder to meet because it arrives on top of unfinished work. MTD rewards businesses that maintain momentum and punishes businesses that rely on last-minute rescue missions.

Common Mistakes

Most MTD mistakes are not technical. They are assumptions. People assume MTD for VAT and MTD for Income Tax are the same thing. They assume a spreadsheet is always fine. They assume their accountant will quietly sort everything without needing better records from them. They assume thresholds are based on profit, not gross income. Nearly every painful MTD conversation starts with one of those misunderstandings.

Confusing the old VAT threshold conversation with the new Income Tax thresholds.

Thinking quarterly updates mean quarterly tax payments.

Assuming gross income and profit are interchangeable for MTD purposes.

Waiting until the first deadline is close before choosing software.

Keeping records digitally in one place, then manually re-keying the numbers somewhere else.

Believing compliance is purely the accountant's problem when the records themselves are not being maintained properly during the year.

The survival strategy is not cleverness. It is rhythm. Connect the bank feed. Keep invoices current. Categorise expenses regularly. Review the books before each quarter ends, not after the deadline has already passed. The less drama there is in the process, the less oppressive MTD feels.

Who Needs To Act Now

Act now if

You are a sole trader or landlord with qualifying income above £50,000

You are VAT-registered but still rely on spreadsheets and manual transfers between systems

You have both self-employment and rental income and have never combined them for MTD threshold purposes

You do not yet have compatible software set up and connected to current records

You want a simple, low-friction route into compliance without taking on a large monthly software cost

You have some runway if

Your qualifying income is below £50,000 and you will not enter the next phase until later

You are a limited company director with no self-employment or property income in scope

You already file VAT digitally and maintain clean, current records throughout the year

You are below the threshold today but want to use the extra time to build a system before it becomes mandatory

You want to test a free MTD-focused setup, such as Sage's free sole trader or landlord route, before the pressure rises

The Bottom Line

Making Tax Digital feels confusing largely because the official language is procedural while the real-world problem is behavioural. HMRC talks about quarterly updates, final declarations, and compatible software. Business owners experience a more basic problem: they want to know whether their current setup is good enough and what they need to change without making life harder than it already is.

The honest answer is that MTD is not trivial, but neither is it the nightmare it is often made out to be. For a business with live digital records and decent software, it is mostly a change in cadence. For a business still running on memory, paper, and year-end improvisation, it is a forced upgrade.

That is why software choice matters more than the marketing around it. The right platform does not just let you submit to HMRC. It reduces hesitation, keeps records current, and removes enough friction that compliance becomes routine. For many UK sole traders and landlords, that is exactly why Sage's free MTD path is likely to be so appealing: it lowers both the technical barrier and the psychological one. And when a tax change is already annoying people, that is not a small advantage.