Hafiza Ayesha Waheed

Hafiza Ayesha Waheed

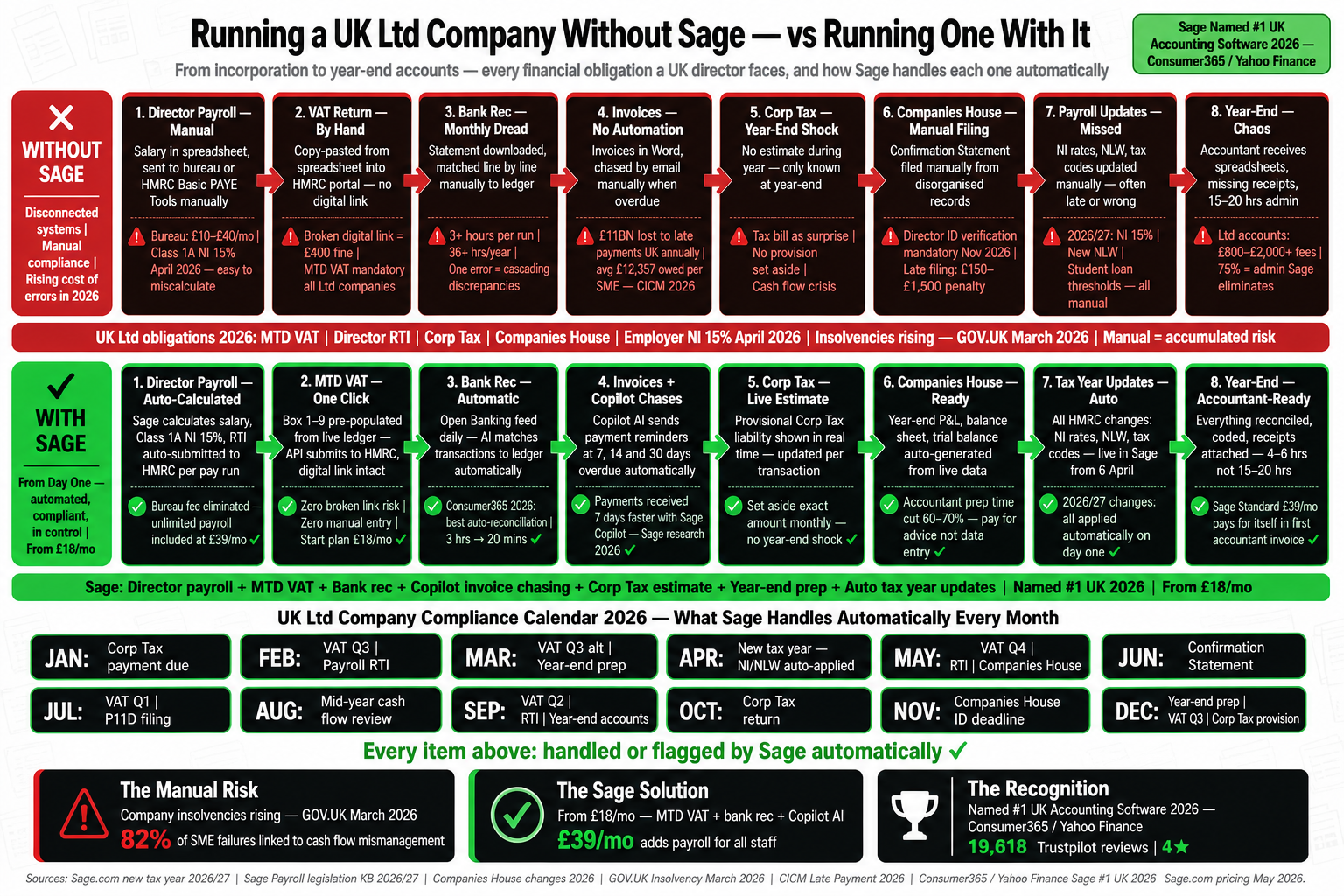

Running a UK limited company feels like a different category of responsibility from being self-employed, and it is. The moment your company is incorporated at Companies House, a compliance clock starts ticking on multiple fronts simultaneously: annual accounts to Companies House, a Corporation Tax return to HMRC, a Confirmation Statement, VAT returns if you are registered, PAYE and RTI submissions if you have employees, and your own Self Assessment as a director. None of these are optional and none of them work on the same deadline. Get one wrong and the penalties apply automatically, without warning, from the day after the missed date.

There is also a change that came into effect on 1 April 2026 that every limited company director in the UK needs to understand: HMRC’s online portal for filing Company Tax Returns closed permanently on 31 March 2026. From 1 April 2026, Company Tax Returns must be filed using commercial accounting software. This is not a gradual transition. It is a hard cut-off. If your company is currently relying on HMRC’s free online service, that service no longer exists. Software is now mandatory for every UK limited company filing a Corporation Tax return. This article explains what that means, what Sage costs for a limited company at every size, and why Sage — from £18 per month for small limited companies up to Sage 50 from £77 per month for more complex businesses — is the platform that makes the compliance side of running a UK Ltd company manageable from day one.

What Running a UK Ltd Company Actually Requires

The compliance obligations of a UK private limited company are more extensive than most new directors anticipate. They do not arrive in one go at the end of the year. They run on different cycles, governed by different bodies, with different penalty structures for non-compliance. Understanding the full picture is the first step to understanding why accounting software is not a convenience for a limited company — it is the infrastructure that keeps everything on track.

Obligation | Who Requires It | Deadline | Penalty for Non-Compliance |

|---|---|---|---|

Annual Accounts (first year) | Companies House | 21 months after incorporation date | £150 automatic penalty; rises to £375 after 1 month, £750 after 3 months, £1,500 after 6 months |

Annual Accounts (subsequent years) | Companies House | 9 months after financial year end | As above — penalties apply from day one past deadline |

Confirmation Statement | Companies House | Within 14 days of the 12-month anniversary of last statement | Company can be struck off the register if not filed; criminal offence for directors |

Corporation Tax payment | HMRC | 9 months and 1 day after accounting period ends | Interest charged from day one after deadline; 5% surcharge if unpaid 6 months later |

Company Tax Return (CT600) | HMRC — software only from 1 April 2026 | 12 months after accounting period ends | £100 immediate penalty; rises to £200 after 3 months; 10% of tax due after 6 months; further 10% after 12 months |

MTD for VAT (if VAT-registered) | HMRC | 1 calendar month and 7 days after each VAT period | Points-based: £200 penalty at threshold; £400 per return for non-compatible software |

PAYE / RTI (if employing staff) | HMRC | On or before each payment date | Penalties from first failure; daily interest on unpaid PAYE from due date |

Director Self Assessment | HMRC | 31 January each year | £100 immediate; then £10/day for up to 90 days; then 5% surcharges at 3, 6, 12 months |

The number of separate obligations, separate deadlines, and separate penalty structures is the primary reason accountants consistently tell new limited company directors to get proper accounting software before they do anything else. Managing these obligations manually — in a spreadsheet, a diary, and a folder of bank statements — is technically possible and practically disastrous. The deadlines do not align, the figures feed into each other, and a single missed date in one obligation can trigger penalties while simultaneously creating incorrect data for the obligations downstream from it.

The April 2026 Change That Makes Software Non-Optional

The closure of HMRC’s online Company Tax Return service on 31 March 2026 is the single most significant compliance change for UK limited companies in recent years, and it received far less attention than it deserved. From 1 April 2026, there is no HMRC portal for filing a CT600. Companies House confirmed the change directly on their official Facebook channel and across their communication channels in the weeks before the deadline. The message was unambiguous: Company Tax Returns must now be filed using commercial software.

This change affects every UK private limited company, regardless of size, profitability, or complexity. A dormant company with no trading activity still has a Corporation Tax return obligation. A company with one director drawing a nominal salary still needs to file. A new company in its first year with minimal transactions still needs software to submit the CT600 that HMRC now requires. The category of “company that can manage without accounting software” effectively ceased to exist on 1 April 2026. The only question remaining is which software, at what price, for what type of limited company.

What this means if your year-end is approaching

If your company’s accounting period ended on or after 1 April 2025, your Company Tax Return deadline falls on or after 1 April 2026 — which means your CT600 must be filed through software, not through HMRC’s portal. If you have not yet set up accounting software or engaged an accountant using software, that deadline is approaching without a compliant submission mechanism in place. The penalty for missing a CT600 deadline is £100 automatically, rising steeply from there.

The Sage Product Range for Limited Companies

Sage’s product range covers limited companies from the smallest single-director consultancy to mid-sized businesses with complex reporting requirements, inventory, multiple departments, and dozens of employees. The entry point for a small limited company is Sage Accounting at £18 per month — the same platform used by many sole traders, but with the features relevant to limited companies fully active, including Corporation Tax support through the accountant integration, VAT returns, and payroll compatibility. For companies with more transactions, more users, or more complex accounting needs, Sage 50 starts at £77 per month and provides the full depth of double-entry bookkeeping, job costing, and reporting that a growing limited company requires.

Product | Monthly Price (excl. VAT) | Best For | Key Capabilities | CT600 Filing |

|---|---|---|---|---|

Sage Accounting Start | £18/mo | New or very small limited companies; single director; simple turnover; VAT-registered | MTD VAT, invoicing, bank feeds, basic P&L and balance sheet, Sage Copilot (1 user), HMRC-compliant records | Via accountant integration; records in Sage, CT600 submitted by accountant using Sage for Accountants |

Sage Accounting Standard | £39/mo | Growing limited companies; cash flow management; receipt capture needed; multiple Copilot users | Everything in Start plus receipt capture (30/mo), cash flow forecasting, additional Copilot users (£20/user/mo) | As above |

Sage Accounting Plus | £59/mo | Limited companies with inventory, product sales, or multi-currency transactions | Everything in Standard plus inventory management, multi-currency, 100 receipt captures/mo included | As above |

Sage 50 Standard | From £77/mo | Established limited companies; higher transaction volumes; multiple users; detailed reporting; job costing | Full double-entry bookkeeping, advanced VAT management, job costing, multi-department, bank feeds, Microsoft 365 integration, detailed audit trail | Direct CT600 filing capability within Sage 50; full Corporation Tax workflow included |

Sage 50 Professional | From £155/mo | Complex limited companies; manufacturing; project accounting; advanced stock management; multiple companies | Everything in Standard plus advanced stock control, project costing, manufacturing modules, multi-company management | Full CT600 filing; multi-company Corporation Tax management |

Sage Payroll Essentials | £10/mo (5 employees included) | Any limited company employing staff; PAYE, NIC, RTI, auto-enrolment pension | PAYE, NIC calculations, HMRC RTI submissions, payslips, auto-enrolment, P60 and P11D production; add employees from £2/employee/mo | N/A — payroll product; works alongside Sage Accounting or Sage 50 |

Sage Payroll Standard | £20/mo (5 employees included) | Companies wanting HR features alongside payroll; employee self-service portal; absence management | Essentials plus employee self-service, HR document storage, absence and holiday management; add employees from £4/employee/mo | N/A |

Sage Payroll Premium | £30/mo (5 employees included) | Companies with timesheet-based workers; overtime management; advanced HR workflows | Standard plus timesheet integration, overtime calculations, advanced HR; add employees from £6/employee/mo | N/A |

The Sage Payroll pricing changed from a tiered employee-band model to a per-employee-per-month model in late 2024. Under the current model, each plan includes 5 employees as the base and additional employees are added at a per-employee rate that decreases as headcount grows — creating a genuinely scalable cost structure for companies whose workforce grows over time. A company with 10 employees on Payroll Essentials pays £10 per month for the base plan plus £2 per employee per month for the additional five employees: £10 + £10 = £20 per month total. A company with 20 employees on the same plan pays £10 + (15 × £2) = £40 per month. The pricing scales with the business rather than jumping between fixed tiers.

The Director’s Financial Picture: What Sage Covers

A limited company director in 2026 typically has a more complex personal tax situation than a pure employee or a sole trader. The most common structure — drawing a small salary up to the National Insurance threshold combined with dividends from company profits — creates a personal tax position that involves Employment Income, Dividend Income, and potentially rental income or other sources, all flowing into a Self Assessment return. That return must be filed by 31 January, and the figures within it depend on the accuracy of the company’s accounts, the correct calculation of the dividend voted during the year, and the correct treatment of any director’s loan account movements.

Sage handles all of these as connected rather than separate. The salary processed through Sage Payroll feeds into the company’s P&L automatically. Dividends voted are recorded as a transaction in the company accounts. The director’s loan account is tracked within the nominal ledger. When the company’s year-end arrives, all of those figures are already in Sage in the correct form for the accountant to prepare the annual accounts and CT600 — and for the director’s own accountant to complete the Self Assessment. The alternative — separate payroll software, a separate dividend record, a manually maintained DLA spreadsheet, and year-end figures reconstructed from bank statements — is more expensive in accountant time than the Sage subscription costs in most years.

What “From Day One” Actually Means for a New Ltd Company

The title of this article promises that Sage makes finances easier from day one, and that claim is worth examining honestly rather than leaving as marketing language. The day-one advantage of Sage for a new limited company is not that the software is simpler than alternatives. It is that starting correctly in Sage means the accounting records grow alongside the company in the right format from the first transaction, rather than accumulating in a format that will need to be reconstructed or corrected before the first set of accounts can be prepared.

Opening balance setup — Sage prompts for the company’s opening bank balance, any assets brought into the company, the share capital issued on incorporation, and any initial liabilities. A company that sets these up correctly in Sage on day one has a balance sheet that is accurate from the start. A company that skips this step has accounts that will need retrospective correction — often at significant accountant cost — before the first year-end can be filed.

Chart of accounts configured for a limited company — Sage’s chart of accounts for a limited company includes the nominal codes for share capital, retained earnings, corporation tax provision, dividend payments, and director’s loan account that are specific to limited company accounting. These are not present in a sole trader accounting setup and cannot be improvised in a spreadsheet without risk of misclassification that affects the accuracy of the CT600.

VAT registration from the first return — if the company registers for VAT before or shortly after incorporation, Sage is set up with the VAT registration number and scheme before the first VAT-applicable invoice is raised. Every subsequent transaction is VAT-coded correctly from the outset. There are no historic invoices to retrospectively re-code because the scheme was applied late.

Bank feed connected from account opening — connecting the company’s business bank account to Sage from the day the account is opened means every transaction from incorporation is imported automatically. No transactions are missing. No reconciliation gaps need to be explained. The bank balance in Sage matches the bank balance in the account continuously, not quarterly.

Payroll before the first salary payment — if the director is drawing a salary, Sage Payroll should be set up before the first pay date, with the director registered as an employee, the PAYE scheme registered with HMRC, and the first Full Payment Submission ready to go before the salary hits the bank account. RTI is due on or before the payment date; there is no grace period for new employers.

Sage Accounting vs Sage 50: Which One Does a Limited Company Need?

The most common source of confusion for limited company directors choosing between Sage products is the difference between Sage Accounting (the cloud-based platform at £18 to £59 per month) and Sage 50 (the more established accounting system starting at £77 per month). Both are HMRC-recognised, both handle VAT and payroll, and both serve limited companies. The difference is depth, user capacity, and the complexity of the accounting tasks they are designed to handle.

Sage Accounting (£18–£59/mo) suits you if

You are a new limited company or a small, established one with relatively straightforward trading

You need one or two users in the accounting system at any given time

Your accountant handles the year-end accounts and CT600 using Sage for Accountants — you provide well-maintained records, they file

You want cloud-first access — full functionality from any browser, any device, without a server or local installation

Your primary needs are invoicing, bank reconciliation, MTD VAT, expenses, and a clear P&L and balance sheet in real time

You value Sage Copilot AI for invoice chasing, anomaly detection, and cash flow alerts

Your turnover is below the threshold at which transaction volume makes cloud processing feel slow

Sage 50 (from £77/mo) suits you if

Your company has significant transaction volume — hundreds of invoices per month, multiple stock locations, or complex purchasing workflows

You need multiple simultaneous users with role-based access and a full audit trail of every change

You want to file CT600 directly within your accounting software rather than via an accountant using a separate platform

Job costing, departmental reporting, or project-level profitability analysis is important to your business

You need Microsoft 365 integration — Sage 50 connects directly to Outlook, Word, and Excel

You have or plan to have stock management requirements that go beyond basic product lists

Your accountant or bookkeeper recommends Sage 50 based on the complexity of your ledger

What Sage Costs vs What Non-Compliance Costs

For a small limited company, the total annual cost of Sage Accounting Standard at £39 per month plus Sage Payroll Essentials at £10 per month for one director-employee is £588 per year excluding VAT. That is the all-in cost of a compliant, fully functional accounting and payroll platform that covers MTD for VAT, payroll RTI, bank reconciliation, invoicing, and the records infrastructure needed for year-end accounts. Against that number, consider the penalty landscape for a limited company that manages the same obligations manually and makes the errors that manual systems produce.

Scenario | Penalty | Sage Accounting Standard + Payroll annual cost |

|---|---|---|

Annual accounts filed 1 month late to Companies House | £375 automatic penalty | £588/yr |

CT600 filed 3 months late to HMRC | £200 (£100 + £100 escalation) | |

One missed VAT return (non-compatible software) | £400 fixed penalty | |

Corporation Tax unpaid for 6 months after due date | 5% surcharge on tax owed plus daily interest from day 1 | |

RTI payroll submission missed for 1 month (1–9 employees) | £100 per month | |

Director Self Assessment filed 3 months late | £100 + £10/day for 90 days = £1,000 maximum |

A single missed Companies House accounts deadline costs £375 in automatic penalties — more than seven months of Sage Accounting Standard. A missed VAT return via non-compatible software costs £400 — nearly seven months of the same subscription. These are not edge cases. They are the standard penalties that apply to the most common compliance failures of small limited companies, and they accumulate faster than most directors anticipate when manual systems fall behind during busy trading periods. The case for accounting software is not about efficiency or convenience for a limited company. It is about the penalty exposure that a manual system creates.

Sage Copilot for Limited Companies: The Features That Matter

Sage Copilot, included with all Sage Accounting plans and available within Sage 50, brings AI-powered functionality to limited company finance management that goes beyond the record-keeping and compliance infrastructure. For a director managing the accounts alongside running the business, the features that reduce active time most significantly are the ones that turn reactive tasks into automated workflows.

Automated invoice chasing — Copilot identifies overdue invoices, drafts payment reminders in the company’s tone, and sends them automatically with the director’s approval. Tested cases show payments received an average of 7 days faster, directly improving cash flow without requiring the director to track and chase each debtor manually.

Cash flow alerts — Copilot projects the company’s bank balance forward based on outstanding receivables, known payables, and recurring commitments. Projected shortfalls are surfaced before they occur, giving the director time to act — chase an invoice, delay a purchase, arrange an overdraft facility — rather than reacting after the cash position has deteriorated.

Corporation Tax provision estimate — as transactions accumulate through the year, Copilot maintains a running estimate of the Corporation Tax liability based on current profit. This is the number that catches many directors off guard: the tax is due 9 months and 1 day after the accounting period ends, but the profit that generates it has been accumulating all year. Seeing a real-time estimate throughout the year allows the company to plan for the payment rather than face a surprise.

Anomaly detection — Copilot flags transactions that break established patterns: an unusually large payment to a supplier, a duplicate entry, a VAT rate applied to a transaction that differs from all similar previous transactions. These are surfaced for human review before they affect the accounts, not after the year-end reconciliation reveals them.

Director’s loan account monitoring — overdrawn director’s loan accounts create a Corporation Tax liability under Section 455 if not repaid within 9 months of the accounting period end. Copilot tracks the DLA balance and alerts when the account moves into debit, giving the director the visibility needed to manage repayment timing before the tax charge applies.

The Accountant Relationship: How Sage Makes It Work

Most small limited companies use an accountant for their year-end accounts and CT600 filing, even if the day-to-day bookkeeping is managed internally. The quality of that relationship — and the cost of the year-end work — is directly determined by the quality of the records the accountant receives. An accountant working from a well-maintained Sage file with reconciled bank accounts, correctly categorised transactions, and a clean VAT position can prepare annual accounts in hours. An accountant working from a bank statement, a folder of unsorted receipts, and a spreadsheet that may or may not be accurate requires days — and charges accordingly.

Sage for Accountants, the platform used by Sage-aligned accounting practices, connects directly to a client’s Sage Accounting subscription. The accountant can review the file, make adjusting entries, run the trial balance, prepare the statutory accounts, and file the CT600 without the client needing to export anything or prepare a year-end pack. The records the client has maintained throughout the year become the accountant’s working file directly. For a client paying an accountant £500 to £1,500 per year for year-end services, arriving with clean Sage records rather than manual records typically reduces the year-end bill by £150 to £400 — an amount that covers the Sage Accounting subscription for the entire year in many cases.

The Bottom Line

Running a UK limited company in 2026 involves a compliance burden that has grown consistently in recent years and will continue to do so. The closure of HMRC’s online Company Tax Return service on 31 March 2026 removed the last option for filing a CT600 without commercial software. MTD for VAT has been mandatory since 2022. PAYE RTI has been mandatory since 2013. The common thread across every one of these obligations is that they require digital systems, not manual processes, to be met reliably and at scale.

Sage provides the full infrastructure for a UK limited company’s compliance requirements in a single, connected platform. Sage Accounting starts at £18 per month with two months free for small limited companies that need cloud-based bookkeeping, MTD VAT, invoicing, bank feeds, and Copilot AI. Sage 50 starts at £77 per month for companies that need deeper accounting capability, direct CT600 filing, job costing, or multiple users. Sage Payroll starts at £10 per month for up to five employees, with per-employee pricing for additional headcount that scales as the business grows.

The case for Sage is not that it is the only accounting software for UK limited companies. It is that it is the most complete, the most deeply integrated with HMRC’s compliance requirements, the most used by UK accountants, and the most capable of growing with a company from its first invoice to its hundredth employee — without requiring a platform migration at every growth stage. Starting on Sage on day one means the records are right from the beginning, the compliance infrastructure is in place before the deadlines arrive, and the accountant relationship works with the quality of records that produces the lowest year-end bill. For a limited company director who already has enough to manage without adding an accounting crisis to the list, that is worth considerably more than £18 a month.